Egypt, a country with a population of 90m, where more than 28% of them live below the poverty line, has been suffering following the 25 January Revolution in 2011 from economic challenges and political instability. These factors intensified Egypt’s already-existing structural problems.

Since November 2016, when the authorities started to implement the economic reform programme backed by the International Monetary Fund (IMF), inflationary pressures have been building up because of the Central Bank of Egypt’s (CBE) decision to float the national currency, introducing the value added tax (VAT), and reducing fuel subsidies twice, in order to receive the International Monetary Fund’s (IMF) approval of the $12bn loan.

The road to rampant inflation

The road to rampant inflation

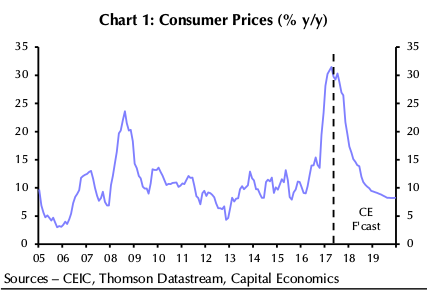

Following the November 2016 decisions made by the CBE, inflation rose sharply, primarily as a result of the devaluation of the Egyptian currency by almost 50%. In December 2016, inflation registered 23.27% and continued its increase to reach its highest level in 30 years—it was somewhere around 31.5% in April, considered to be the highest registered inflation rate of any of the world’s large economies.

Different points of view about the main driver behind inflation and how to deal with it emerged. Various economic experts argued that higher inflation rates were a result of the economic reforms that started by the end of 2016, which fueled a significant increase in prices as the costs of many factors of production are priced in US dollars since they are imported. They concluded that once these price shocks were absorbed, inflation will gradually decline on its own; thus, they were against the CBE’s decision of raising interest rates.

However, many experts, who share the same point of view with the IMF, believe that Egypt’s inflation rate was already among the highest in the world even before such price shocks, according to CBE’s historical data, Egypt’s inflation rate registered at 15.5% in August 2016. In their opinion, the primary driver behind Egypt’s soaring inflation is not the devaluation or fuel price hikes. But the rather rapid expansion of the money supply over the past few years.

Since the 25 January revolution, to prevent more anger among Egyptians, successive governments maintained an unsustainable huge budget deficit driven by weak revenues and large subsidy and wages bills, which they had financed, in effect, by printing money. This has resulted in too much cash accompanied by decline in production of goods and services, pushing prices up.

Moreover, such expansion of the money supply was one of the reasons behind the decline in the value of the Egyptian pound to fall against the dollar, leading to a currency crisis and to a huge gap between the value between the official and unofficial foreign exchange rates. This is why the CBE was forced to devalue in November.

Moreover, such expansion of the money supply was one of the reasons behind the decline in the value of the Egyptian pound to fall against the dollar, leading to a currency crisis and to a huge gap between the value between the official and unofficial foreign exchange rates. This is why the CBE was forced to devalue in November.

Egypt’s domestic liquidity, which is the amount of Egyptian pounds in circulation or in-demand deposits, witnessed a 4.68% increase in March to a total of EGP 2.75tn. During the same period, GDP growth was lower than 4%. It is arguably a classic case of stagflation, and it needs to be addressed as quickly as possible.

Raising interest rates was the solution advised by the IMF and many other experts to tackle this problem. Consequently, the CBE decided to raise the interest rates in June for the third consecutive time, following the recently implemented energy subsidy cuts increasing its overnight deposit rate to 16.75% from 14.75% and its overnight lending rate to 17.75% from 15.75%, making the total interest rate hike of 7% since November an effort to curb the skyrocketing high inflation rates so that it would be in line with the authorities’ goal to reach a single-digit inflation rate in 2019.

In the CBE’s accompanying statement, the Monetary Policy Committee (MPC) explained that the move to raise rates came as a response to concerns over the inflation outlook, as the balance of risks surrounding the inflation outlook has tilted more strongly to the upside with the recent economic and monetary developments.

The move was welcomed by some and objected by many. HSBC published a report stating that this move is a source of comfort, as it shows the CBE’s solid efforts and commitment to contain inflation and to re-establish its credibility in targeting inflation in the context of the broader economic reform programme.

On the other hand, Prime Holding economist Eman Negm argued against this decision, explaining that such interest rate hikes can have a negative effect on inflation, as it will increase the borrowing costs for companies, leading to an increase in production costs.

Moreover, a soaring inflation rate has taken its toll on the consumer purchasing power. This, in turn, has led to a decline in demand rates, increasing the risk of recession with rising prices (stagflation). According to Emirates NBD Egypt PMI data, the Egyptian economy is a continued contraction route, with monthly readings registering below the 50-point threshold for the twentieth month in a row, through May 2017. This contraction, which sharply increased after the pound flotation, was due to the decline in output and new orders.

Moreover, a soaring inflation rate has taken its toll on the consumer purchasing power. This, in turn, has led to a decline in demand rates, increasing the risk of recession with rising prices (stagflation). According to Emirates NBD Egypt PMI data, the Egyptian economy is a continued contraction route, with monthly readings registering below the 50-point threshold for the twentieth month in a row, through May 2017. This contraction, which sharply increased after the pound flotation, was due to the decline in output and new orders.

Nevertheless, there was a decrease in output and new orders in June 2017, but contraction has slightly eased as a result of the increased new export orders benefiting from the currency devaluation. New export orders have been on the rise since April 2017, recording an expansion for the first time in almost two years. This then rose in May at the fastest rate since the inception of the PMI in April 2011.

However, rising interest rates, by 7 pp after flotation, have led to a rise in both the cost of debt and the cost of equity. Thus, the weighted average cost of capital (WACC) has increased from 23.6% before the flotation to 26.2% after the flotation, reducing the investment attractiveness of the Egyptian market.

Moreover, one of the main criticisms of CBE’s Thursday interest rate hike is that it will make it more expensive for businesses to invest at a moment when the economy is suffering and desperately needs the stimulus. But this point view is objected by the fact that most Egyptian banks’ funding and lending have been directed to the government, helping in financing the huge deficit at hand through T-bills and government bonds, with low lending directed to private businesses.

To conclude, either way the average Egyptian citizen will carry the burden of the adopted reforms, with the expected increase in Egypt’s inflation rate by an approximate 3-4.5 percentage points following last week’s fuel price hike, according to Deputy Finance Minister Ahmed Kojak.